Outsmart your car insurance renewal notice: 4 things to renegotiate before you sign your next policy

Suppose you are a seasoned car owner, then you must be through with the drill. It happens every year, like clockwork. So, you open your inbox, and there it is: a notice from your car insurance provider regarding policy renewal. Do you know what 90% of car owners do in such a scenario? They simply sigh, pull out the credit card, pay the premium, and get it over with. And why not? It's convenient, it's fast, and the agent makes it incredibly easy, as the client just needs to say "yes."

KEY TAKEAWAYS

Is the insurance renewal quote sent by my agent always final?

Not at all. The initial renewal notice is essentially an opening offer. Your agent usually has flexibility with discounts, add-on adjustments, and promotional perks to keep a loyal client from switching to a competitor. So, take advantage of the renewal period.What happens to my No-Claim Discount (or No-Claim Bonus) if I switch to a different insurance company?

Do not worry, you won’t lose it! Your NCD reflects your history as a safe driver, not just your loyalty to one company. If you decide to change providers, request an NCB certificate from your current insurer and present it to the new one. This will help you claim discounts or other perks depending on the provider.Will raising my Third-Party Property Damage (TPPD) limit double my premium?

Surprisingly, no. Because the statistical likelihood of rear-ending a luxury vehicle is relatively low, increasing your TPPD limit from a basic level to a much higher tier usually only adds a few hundred pesos to your total annual cost.Can I negotiate my policy mid-year, or do I have to wait for the renewal notice?

Technically, you can modify your policy or cancel it at any time. However, the renewal window is when you have the absolute maximum leverage. This is when your insurer is actively working to prevent you from shopping around.What is the difference between Compulsory and Voluntary Third-Party liability?

Compulsory Third-Party Liability (CTPL) is required by law to register your vehicle and primarily covers bodily injury or death of a third party. Voluntary TPPD is an optional layer of your comprehensive policy that covers damage you cause to property (such as another person's car or a gate).If I drive very little now, can I get a mileage-based discount?

Yes,a couple of digital-first platforms offer pay-how-you-drive programs. For instance, if your daily commute has turned into a permanent work-from-home setup, bring this up during your renewal; it might qualify you for a reduced rate.Save Up to 60% on Car Insurance Renewal

- CASA Coverage Up To 10 Years Old

- Free Roadside Assistance

- Free Acts of God/Acts of Nature

T&C

T&C

But here is the truth: when you blindly accept the first quotation that comes your way, you are not only losing your hard-earned money but also better protection on the table.

Insurance companies, whether national or international players, operate the same way and are very well aware of your desire for convenience.

Also, they know about your hesitance to challenge the figures mentioned in the renewed policy. But you should know that the arrival of the car insurance renewal notice marks the moment when your bargaining power is strongest. As a reliable, current policyholder, you have the advantage because the insurer is eager to retain your business.

So, the next time you receive the renewed car insurance policy, make sure to flip the script. Here are four things you need to renegotiate to get the coverage you actually deserve.

Also Read: Common myths around total loss car insurance & the truth behind them

1. Strip away the ghost add-ons

Insurance policies love to hike the price in the name of extra coverage — those little extra add-ons surely sound great in theory, but do absolutely nothing for you in reality. Over time, your driving habits change, but your policy stays exactly the same. And it’s high time to make a few necessary changes.

What should you do? Take a hard look at your policy, the coverage it offers, and your requirements. For instance, are you paying for a Passenger Personal Accident add-on (that covers passengers in the car) even though you commute alone 99% of the time? Are you paying for loss-of-use coverage (which pays for a rental car while yours is being repaired) even though you have a spare vehicle?

If such is the case, just call your agent and tell them to strip away the unnecessary. And just like that, you’ll only pay for what is required.

Also Read: What is legal assistance car insurance coverage? A must-read guide for car owners

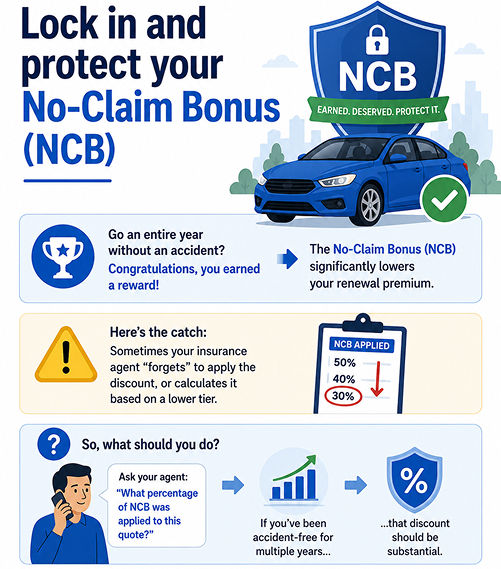

2. Lock in and protect your No-Claim Bonus (NCB)

AI-Generated Image

AI-Generated ImageLet’s say you managed to go an entire year without hitting another car or getting into a fender bender. Congratulations, you have earned yourself a reward. This comes in the form of a No-Claim Bonus (NCB), which significantly lowers your renewal premium.

But here’s the catch: sometimes your insurance agent "forgets" to apply the discount, or they calculate it based on a lower tier.

So, what should you do? Don't just look at the final premium number; ask your agent, "What percentage of NCB was applied to this quote?" If you’ve been accident-free for multiple years, that discount should be substantial.

Also Read: Your weekend road trip insurance checklist: 10 smart steps for a stress-free drive

3. Bump up your Voluntary TPPD (especially for metro traffic)

Let’s take a reality check for when you are driving in dense, chaotic metro areas like Metro Manila. In a basic policy, the standard, bare-minimum Voluntary Third-Party Property Damage (TPPD) coverage limit is often low.

Now, imagine you are moving in packed traffic and accidentally rear-end a brand-new luxury SUV or a sports car. That basic TPPD coverage limit on your policy offers will vanish before the tow truck even arrives, leaving you personally responsible for the rest of the damages.

What to do? When you renegotiate, ask your provider to raise your Voluntary TPPD coverage limit. The beautiful secret here is that bumping your property damage coverage up to ₱500,000 or even ₱1,000,000 costs a surprisingly tiny fraction of your overall premium. It is the cheapest piece of mind you can buy.

Also Read: Common insurance myths Filipino drivers still believe in 2026

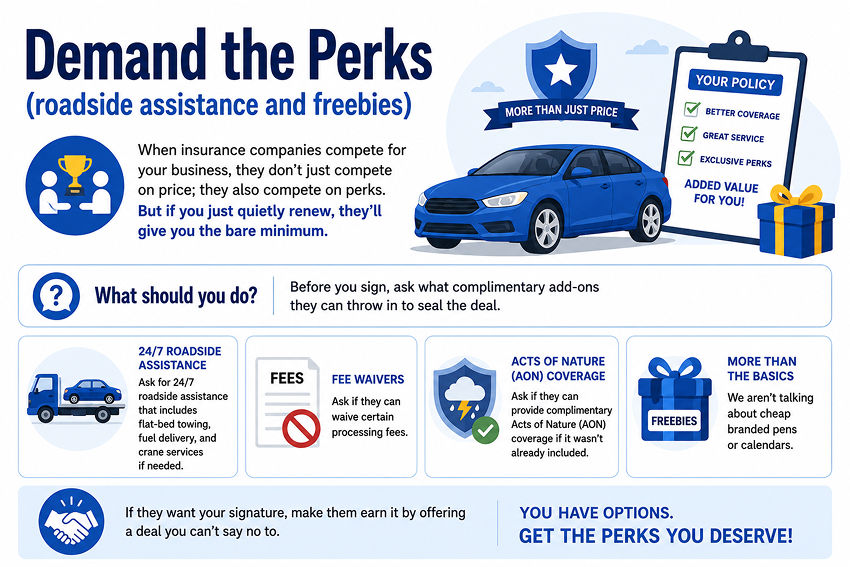

4. Demand the Perks (roadside assistance and freebies)

AI-Generated Image

AI-Generated ImageWhen insurance companies compete for your business, they don't just compete on price; they also compete on perks. But if you just quietly renew, they’ll give you the bare minimum.

What should you do? Before you sign, ask what complimentary add-ons they can throw in to seal the deal. We aren’t talking about cheap branded pens or calendars. For instance, ask for 24/7 roadside assistance that includes flat-bed towing, fuel delivery, and crane services if needed. Ask if they can waive certain processing fees or provide complimentary acts of nature (AON) coverage if it wasn't already included. If they want your signature, make them earn it by offering a deal you can’t say no to.

Also Read: Notarised affidavit in car insurance: Everything a car owner/policyholder needs to know

Bottom line

Your insurance policy is a crucial aspect of your car ownership; it shouldn't be a set-it-and-forget-it subscription. It’s a financial contract, and like any contract, it is entirely open to negotiation.

All you need is just 15 minutes - go through your policy and challenge your renewal notice. This will not just save you a bit of cash; it will also ensure your coverage reflects your life today.

So, the next time that notification pops up, don’t just pay. Pick up the phone, ask the right questions, and be the smartest driver on the road.

Also Read: Acts of Nature coverage: What you need to know in 2026

Featured Articles

- Latest

- Popular

-

-

Acts of Nature coverage: What you need to know in 2026Carmudi PH . May 22, 2026

-

-

-

-

Recommended Articles For You

You Might Also Be Interested In

- Journal

- Advice

- Financing

-

BYD introduces Sealion 7 in PHRuben Manahan IV . May 28, 2026

-

-

10th PIMS: 10 things to watch out forPaulo Papa . May 25, 2026

-

CAMPI-TMA Apr. 2026 sales drop by 12%Ruben Manahan IV . May 25, 2026

-

GAC PH expands lineup with Aion UT introductionRuben Manahan IV . May 21, 2026

-

-

How to handle a checkpoint: The right and wrong movesCarmudi PH . Apr 14, 2025

-

-

-

-

-

Fast-track your car loan payoff with these hacksCarmudi PH . Apr 06, 2025

-

-

-

Need better auto loan terms? Here’s how to refinanceCarmudi PH . Mar 21, 2025

Featured Cars

- Latest

- Upcoming

- Popular

Car Articles From Zigwheels

- News

- Article Feature

- Advisory Stories

- Road Test

-

Mitsubishi Motors PH to unveil all-new Outlander at PIMS 2026?Ruben Manahan IV . Today

-

Subaru PH to bring Crosstrek e-Boxer HybridRuben Manahan IV . Today

-

Geely Motor PH rolls out ‘Your Next Phone Could Be Your Next Ride’ rafflePaulo Papa . Today

-

Suzuki Cars PH to showcase eVitara at PIMS 2026?Cesar Miguel . May 28, 2026

-

In 10 pictures: BYD Cars PH unleashes Sealion 7 performance SUVPaulo Papa . May 28, 2026

-

3 reasons to buy the BYD Sealion 7 EVCesar Miguel . Today

-

Here are the Dongfeng Vigo’s strengths, weaknessesCesar Miguel . May 27, 2026

-

3 reasons to be excited about the Toyota Land Cruiser FJCesar Miguel . May 26, 2026

-

Here are the GAC Aion UT’s 2 closest rivalsCesar Miguel . May 25, 2026

-

Check out the Toyota bZ4X's 4 electrifying tonesPaulo Papa . May 20, 2026

-

Tips on how to prevent vehicle firesCesar Miguel . Mar 17, 2026

-

How to prepare your car for summerCesar Miguel . Mar 11, 2026

-

Avoid road trip horror stories this 'Undas' with these tipsRuben Manahan IV . Oct 20, 2025

-

Here are ways to avoid road ragePaulo Papa . Sep 23, 2025

-

How well do you understand traffic signs?Cesar Miguel . Sep 09, 2025

-

ELECTRIA: VinFast VF 6 is a well-equipped urban warriorCesar Miguel . Apr 20, 2026

-

BYD DM-i lineup conquers Southern LuzonCesar Miguel . Mar 10, 2026

-

Hyundai Creta Premium: balancing engaging drive,comfortCesar Miguel . Feb 13, 2026

-

First drive: 4th-gen Changan CS55 PlusPaulo Papa . Feb 09, 2026

-

Changan CS15: small upgrades makes the differenceCesar Miguel . Feb 06, 2026